Introduction

Running a business with two or more legal entities is a different challenge altogether from managing a single company. As Indian MSMEs expand into subsidiaries, franchise locations, or holding structures, their existing accounting systems start showing cracks: consolidated financials become a manual ordeal, and GST compliance across entities multiplies fast.

That's where multi-entity management comes in — the structured approach to running the financial, operational, and compliance activities of two or more legally distinct business units under shared ownership. When handled well, it gives leadership a clear, group-level view of performance without losing sight of how each entity is doing on its own.

This guide covers what multi-entity management actually involves, how the consolidation process works step by step, the challenges that derail most finance teams, and which business structures genuinely need it.

Key Takeaways

- Multi-entity management governs finances, compliance, and reporting across multiple legal entities from one central point

- Financial consolidation combines each entity's data into one group view — while removing internal transactions that would inflate revenue or expenses

- Without a structured process, businesses face delayed closings, intercompany mismatches, and missed GST or MCA filing deadlines

- For Indian MSME finance teams, a unified platform replaces the slow export-and-merge cycle with real-time, entity-level visibility

- This guide explains the process, the pitfalls, and which businesses actually need it

What Is Multi-Entity Management?

Multi-entity management is the structured framework through which a parent organisation oversees the financial records, reporting, compliance, and intercompany activity of all its subsidiary entities or business units. Each entity keeps its own books; the framework binds them into a coherent group picture.

The goal is a single, accurate consolidated view of group financial health, produced without double-counting internal transactions and without losing entity-level detail. Both requirements matter: group leadership needs the consolidated picture; auditors, regulators, and operating managers need entity-level accuracy.

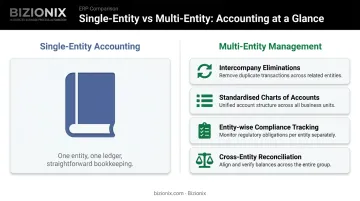

How It Differs from Standard Accounting

Single-entity accounting manages one legal unit in isolation. Multi-entity management coordinates multiple independent ledgers into a coherent group-level picture. That coordination requires steps that simply don't exist in single-entity work:

- Intercompany eliminations — removing transactions between related entities from consolidated statements

- Standardised charts of accounts — ensuring all entities use consistent account codes and categorisation logic

- Entity-wise compliance tracking — monitoring separate GST registrations, TDS obligations, and filings per entity

- Cross-entity reconciliation — verifying that intercompany balances match on both sides before consolidation begins

The burden of each step compounds as entity count grows — what takes hours across three entities can consume weeks across ten without the right systems in place.

Why Multi-Entity Financial Consolidation Matters for Growing Businesses

When a business operates multiple entities without a unified system, finance teams spend days manually exporting data, reconciling mismatches, and assembling reports. The result is a close cycle that is slow, error-prone, and useless for real-time decisions.

The Intercompany Problem

Intercompany transactions (internal loans, shared service charges, goods transferred between entities, management fees) must be identified and removed from consolidated statements. When they aren't, the group appears to have more revenue and more expenses than it actually generates with external parties.

According to BlackLine's 2023 survey of 263 intercompany stakeholders, 99% reported specific intercompany process challenges, and 97% had to resolve multi-million-dollar material variances. These aren't niche problems — they're the norm for any organisation managing internal transactions across entities without automated matching.

The Compliance Dimension for Indian Businesses

Under India's GST framework, registration is state-specific and PAN-based: one GSTIN per state. A business with operations in five states holds five separate registrations, each with its own GSTR-1 and GSTR-3B filing obligations.

Managing these independently across entities creates real regulatory risk: missed deadlines, inconsistent reporting between entity-level and consolidated books, and late fees under Section 47 of the CGST Act.

Additionally, Section 129(3) of the Companies Act, 2013 requires any company with one or more subsidiaries to prepare consolidated financial statements in addition to standalone statements — making consolidation a legal requirement for holding-subsidiary structures, not just an operational preference.

The Decision-Making Cost

Without a real-time consolidated view, CFOs and business owners are flying blind on questions that directly affect the business:

- Which entities are cash-positive and which need liquidity support

- Whether group-level profitability masks underperforming subsidiaries

- Where capital should be redeployed for the highest return

Delayed, piecemeal data doesn't just slow decisions — it distorts them. Capital gets misallocated, liquidity gaps go unnoticed, and risk accumulates before anyone has a complete picture.

How Financial Consolidation Works in a Multi-Entity Setup

The consolidation process follows a consistent sequence: each entity maintains its own ledger and produces its own trial balance; these are aggregated, mapped to a common chart of accounts, adjusted for intercompany activity, and combined into group-level financial statements.

The output is a consolidated P&L, balance sheet, and cash flow statement that accurately represents total group performance, free from distortions caused by internal transactions.

Step 1: Entity Setup and Chart of Accounts Standardisation

Before consolidation can happen, every entity's accounting structure must use a common framework — standardised account codes, consistent revenue recognition policies, and aligned reporting periods. Without this, data from different entities can't be meaningfully compared or combined.

The common failure is allowing entities to develop their own account structures, then facing enormous remapping effort at every close. Standardising upfront eliminates this recurring friction. Under Ind AS 110, which governs consolidated financial statements in India, uniform accounting policies are mandatory for like-for-like transactions across group entities.

Step 2: Recording and Managing Intercompany Transactions

Intercompany transactions must be recorded identically on both sides — as a payable in one entity and a receivable in the other. This symmetry is what makes clean reconciliation possible later.

When this step is done manually or inconsistently, mismatched entries create reconciliation problems at month-end. One entity records a management fee as an expense; the other hasn't recorded the corresponding income. Those mismatches compound across dozens of transactions and delay the entire closing process.

Step 3: Consolidation, Eliminations, and Unified Reporting

Once entity data is aggregated, all intercompany activity must be removed from the consolidated statements before the group financials are meaningful. This elimination step is where consolidation becomes technically demanding, and where manual processes break down most visibly.

Items that must be eliminated include:

- Intercompany receivables and payables

- Revenue billed from one group entity to another

- Expenses recharged between entities (management fees, shared costs)

- Unrealised profits on internal sales

A platform like Bizionix supports this process through multi-company management under a single login, giving finance teams access to both consolidated and entity-level views without manual exports. Each entity maintains independent books with separate GST, compliance, ledgers, and financials, while group-level dashboards aggregate the data in real time.

Key Challenges in Multi-Entity Financial Consolidation

Intercompany Complexity

Intercompany transactions are the most common source of consolidation errors. When entities conduct dozens of internal transactions monthly without an automated matching system, finance teams must manually verify that every entry appears correctly on both sides. BlackLine's 2024 finance survey found 68% of respondents said manual work leaves organisations vulnerable to errors that undermine business decision-making — and intercompany reconciliation is one of the most manual-intensive processes in multi-entity finance.

Data Inconsistency Across Entities

When entities use different accounting methods, different systems, or different categorisation logic, aggregating their data requires extensive remapping. This is particularly common in Indian MSMEs where different branches may run on different tools or maintain spreadsheet-based records. Inconsistent data makes it impossible to compare entity performance on a like-for-like basis — even after the data is pulled together.

Compliance Fragmentation

In a multi-entity Indian business, each entity carries its own GST registration, separate TDS filings, and distinct state-level obligations. Managing these in isolation — without a centralised view — creates real risk:

- Missing filing deadlines across entities

- Inconsistencies between entity-level and consolidated accounts

- Duplicate entries that distort the group view

The GSTN reported over 14.7 crore active taxpayers as of August 2024, with GSTR-3B filing rates between 88.55% and 91.37% — meaning roughly 1 in 10 filings are missed in any given period.

The Spreadsheet Misconception

The compliance and data challenges above don't get easier with spreadsheets — they get harder. Many growing businesses assume spreadsheet-based consolidation is adequate for smaller multi-entity groups, but it degrades quickly as transaction volumes and entity counts grow.

What feels manageable with three entities becomes genuinely unworkable at eight. Formula dependencies multiply, version control collapses. A single miscategorised entry can corrupt the entire consolidated view.

Who Needs Multi-Entity Management and When

Business Structures That Require It

Multi-entity management is necessary for:

- Holding-subsidiary groups — especially those subject to Companies Act Section 129(3) consolidation requirements

- CA firms managing multi-company client portfolios — where a single practice oversees distinct legal entities for multiple clients

- Franchise networks — where each location may be a separate legal entity with shared ownership

- Multi-location manufacturers and distributors — with separate regional entities and intercompany supply chains

- Hotel and resort chains — where individual properties operate as distinct entities under common ownership

- Multi-state businesses — managing separate GST registrations and state-specific compliance obligations

When It Becomes Necessary

The trigger is not entity count alone. Multi-entity management becomes necessary when:

- Two or more entities begin transacting with each other

- Group-level reporting is needed by investors, lenders, or leadership

- Compliance across multiple GST registrations or legal structures becomes too complex to manage manually

- Leadership needs a real-time consolidated view that spreadsheets can't provide

When It's Overkill

Not every multi-entity situation warrants a consolidation framework. A business with two completely independent entities that share no ownership, no internal transactions, and no consolidated reporting requirements does not need intercompany elimination workflows or a group consolidation process.

The right test is whether there is a genuine need for a unified financial picture across entities — not whether multiple entities happen to exist under the same individual's ownership.

For Indian MSMEs that do cross that threshold, Bizionix's multi-company management module covers the essentials: single-login access, entity-wise accounting with independent GST and compliance records, and group-level dashboards sized for growing businesses rather than enterprise ERP deployments.

Frequently Asked Questions

What is multi-entity management?

Multi-entity management is the process of administering the finances, compliance, and reporting of two or more legally distinct business units under common ownership. It uses a structured framework that maintains entity-level detail while enabling a consolidated group-level view across the entire organisation.

What is entity management?

Entity management refers to the ongoing governance of a single legal business unit's financial records, compliance filings, and operational data. Multi-entity management extends this to coordinate multiple such units under one framework.

What is the difference between multi-entity accounting and single-entity accounting?

Single-entity accounting manages one legal unit in isolation. Multi-entity accounting must maintain separate books per entity and produce consolidated group statements — requiring additional steps like intercompany elimination, standardised charting, and cross-entity reconciliation that don't exist in single-entity work.

What are intercompany eliminations and why do they matter?

Intercompany eliminations are the accounting adjustments that remove internal transactions between related entities from consolidated statements. They prevent double-counting of revenue and expenses that would otherwise inflate group figures beyond what external trading alone would justify.

How do Indian businesses with multiple GST registrations manage financial consolidation?

Each entity's GST obligations are tracked separately at the entity level, with its own GSTIN, filing schedule, and compliance records. A unified platform like Bizionix allows finance teams to maintain this entity-wise separation while aggregating data for group-level reporting. This reduces the risk of missed filings or inconsistencies between statutory and management accounts.

When should a growing Indian MSME start using multi-entity management?

The right time is when two or more entities begin transacting with each other, when group-level reporting is needed by investors or leadership, or when compliance across multiple GST registrations becomes too complex to manage with spreadsheets.