This article explains how invoice matching works under GST, the step-by-step process from GSTR-1 to GSTR-3B, the difference between 2-way, 3-way, and 4-way matching, and the common mistakes that cost businesses real money.

Key Takeaways

- Invoice matching cross-verifies a supplier's GSTR-1 data against a buyer's inward supply records to confirm ITC eligibility

- Six fields must match exactly: supplier GSTIN, buyer GSTIN, invoice number, invoice date, taxable value, and tax amount

- If records don't match, the buyer cannot claim ITC — even if the transaction was legitimate

- GSTR-2 matching has been suspended since 2017; the Invoice Management System (IMS), live since October 2024, is now the active system handling this process

- Integrated ERP software reduces mismatch risk by syncing GST data automatically before invoices reach the compliance cycle

What Is Invoice Matching Under GST?

Invoice matching is the process by which the GSTN compares taxable supply details filed by a supplier against the inward supply records of the buyer. Every time a supplier uploads an invoice via GSTR-1, that data travels through the GST portal infrastructure and appears in the recipient's dashboard — creating a linked digital trail between two registered parties.

The purpose is specific: ITC can only be claimed on invoices that the supplier has legitimately uploaded. This prevents fraudulent credit claims, duplicate ITC, and tax leakage across the supply chain.

This compliance mechanism is distinct from internal invoice reconciliation — a check you run inside your own books. Invoice matching is governed by the GSTN itself, with direct consequences for ITC eligibility under the CGST Act. The distinction matters because:

- Internal reconciliation catches discrepancies in your own records

- Invoice matching determines whether ITC is legally claimable

- Mismatches flagged by the GSTN can trigger ITC denial or reversal

Why Invoice Matching Is Critical for ITC Claims

Under Section 16(2)(aa) of the CGST Act, a buyer can claim ITC only if the supplier has furnished the corresponding invoice details in their outward supply statement, and the GST portal has communicated those details to the recipient. In practice, your supplier's filing behaviour directly controls your ITC eligibility.

The scale of the problem is significant. According to a PIB press release from the Ministry of Finance, CBIC Central Tax formations detected ₹36,374 crore of fake ITC across 9,190 cases in FY 2023-24 alone — up from ₹24,140 crore in FY 2022-23. Invoice matching is the government's primary tool to close this gap — and for businesses, failing that match has direct financial consequences.

What Failed Matching Costs Your Business

When invoice matching fails, the consequences compound quickly:

- ITC is denied for that invoice period — even if you paid GST to the supplier

- Working capital gets blocked, particularly for businesses with high purchase volumes

- GST compliance ratings drop, which can trigger scrutiny during assessments

- Tax notices and penalties may follow if ITC is claimed without GSTR-2B support

- Time limit risk: Section 16(4) bars ITC after 30 November following the relevant financial year, leaving a hard deadline to resolve mismatches

Rule 36(4) confirms this directly: businesses cannot claim ITC unless the supplier has furnished invoice details in GSTR-1 or IFF and those details appear in the recipient's GSTR-2B. No exceptions apply.

How the Invoice Matching Process Works Under GST

The matching process follows a defined sequence each month. Each step builds on the previous, and a gap at any stage can disrupt ITC eligibility.

Step 1: Supplier Files GSTR-1 by the 11th

The supplier uploads all outward supply invoices via GSTR-1 (or IFF for quarterly filers) by the 11th of the succeeding month. Once saved or filed, these invoices appear immediately in the recipient's IMS dashboard on the GST portal.

Step 2: Recipient Reviews Invoices on IMS Dashboard by the 14th

The recipient views all inward invoices — classified by type: B2B, credit notes, debit notes, and amendments — and takes one of three actions:

- Accept: Invoice is included in GSTR-2B and eligible for ITC

- Reject: Invoice is excluded from ITC for that period

- Pending: Invoice is carried forward to the next period for a decision

Important: If no action is taken by the time GSTR-2B is generated, the system treats the invoice as deemed accepted. This does not guarantee ITC eligibility — the supplier must have filed correctly in GSTR-1 first, and all Section 16 conditions must still be met.

Step 3: GSTR-2B Auto-Generates on the 14th

GSTR-2B is a static statement, generated once on the 14th based on accepted supplier filings. If a recipient changes their IMS action after the 14th, they must recompute GSTR-2B before filing GSTR-3B. The finalised GSTR-2B data pre-fills Table 4 of GSTR-3B, from which ITC is formally claimed by the 20th.

The Six Fields That Must Match

GSTN's Matching Offline Tool compares GSTR-2B against the purchase register. The six critical data fields it checks are:

| Field | What It Captures |

|---|---|

| GSTIN of Supplier | Registered supplier identity |

| GSTIN of Recipient | Registered buyer identity |

| Invoice / Debit Note Number | Unique document identifier |

| Invoice / Debit Note Date | Date of the transaction |

| Taxable Value | Value on which GST is calculated |

| Tax Amount | GST charged (CGST + SGST or IGST) |

A discrepancy in any of these fields can block ITC — even if the transaction itself was completely legitimate.

Businesses running manual reconciliation across spreadsheets and disconnected tools face the highest exposure to these mismatches. This is where upstream data accuracy matters most — errors introduced at the invoicing stage compound through every subsequent step in the matching cycle. Bizionix handles this through direct API integration with the GST e-Invoice system, which auto-validates invoice data before submission and auto-populates GSTR-1, so supplier-side data is clean before it reaches the buyer's IMS dashboard.

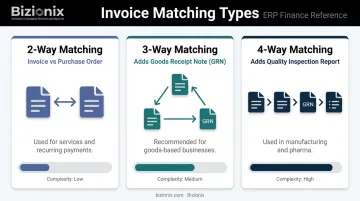

Types of Invoice Matching in GST: 2-Way, 3-Way, 4-Way, and IMS

While the GST portal uses document-level matching through IMS and GSTR-2B, businesses also apply internal matching controls before approving invoices for payment. These internal controls — 2-way, 3-way, and 4-way matching — are procurement discipline tools, not portal mechanisms.

2-Way Matching

Compares two documents: the supplier invoice against the purchase order (PO). It verifies that price, quantity, and GST amounts match what was ordered and what was billed. Typically used for service purchases or recurring vendor payments where no physical delivery confirmation is needed.

3-Way Matching

Adds a third document: the Goods Receipt Note (GRN), which confirms that goods billed were actually received. This is the recommended standard for most goods-based businesses — it protects against paying for items never delivered and ensures ITC claims reflect actual receipt of supply, as required under Section 16(2) of the CGST Act.

4-Way Matching

Introduces a quality inspection report or acceptance certificate as a fourth verification layer. Used in manufacturing, pharma, or government procurement where quality conformance is a contractual condition before payment approval. Only when goods meet specifications is the invoice approved and ITC claimed.

The Invoice Management System (IMS)

Where internal matching controls govern procurement approvals, IMS is what formalises the match at the GST portal level — between supplier-uploaded invoices and buyer records. It went live in October 2024, with the first IMS-based GSTR-2B generated for the October 2024 return period on 14 November 2024.

Key IMS features:

- Accept / Reject / Pending actions on each inward invoice

- Deemed acceptance on inaction (once GSTR-3B is filed)

- Bulk actions for businesses handling high invoice volumes

- Direct integration with GSTR-2B for eligible ITC

- As of October 2025, a dedicated "Import of Goods" section covering Bill of Entry records from ICEGATE

Note that GSTR-2 filing was deferred in September 2017 and has never resumed. IMS and GSTR-2B are the operative mechanisms for buyer-side reconciliation today — any compliance workflow still referencing GSTR-2 needs to be updated accordingly.

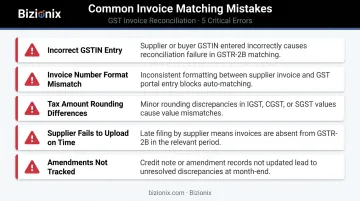

Common Invoice Matching Mistakes and How to Avoid Them

Most matching failures trace back to a small set of preventable errors:

- GSTIN entered incorrectly by either party — a single character difference renders the match invalid

- Invoice number format differences between supplier records and buyer books (spaces, prefixes, or case variations)

- Tax amount discrepancies due to rounding differences between systems

- Supplier fails to upload the invoice in GSTR-1, or uploads it late — the invoice won't appear in GSTR-2B

- Amendments not tracked — if a supplier amends an invoice after filing, the recipient's IMS must reflect the updated version before ITC is confirmed

How to Reduce Matching Failures

Supplier actions:

- Send regular reminders to vendors to file GSTR-1 by the 11th

- Confirm that GSTIN, invoice number, and tax values in your purchase order match what they'll file

Buyer actions:

- Reconcile your internal purchase register against GSTR-2A (dynamic) and GSTR-2B (static) before filing GSTR-3B

- Don't assume deemed acceptance means ITC is confirmed — verify the supplier filed correctly first

- Monitor Section 16(4) deadlines; unclaimed ITC expires

System-level controls:

- Use an accounting platform with GST compliance built in. Bizionix, for example, runs pre-validation checks that catch incorrect GSTIN formats, duplicate invoice numbers, and tax miscalculations before an invoice reaches the portal — preventing errors from showing up as mismatches on the recipient's IMS dashboard.

Frequently Asked Questions

What is invoice matching in GST?

It is the process of cross-verifying a supplier's outward supply details filed in GSTR-1 against the buyer's inward supply records through the GSTN portal. When records align, the buyer's ITC claim for that invoice is confirmed. When they don't, ITC is blocked until the discrepancy is resolved.

Is the Invoice Management System (IMS) mandatory under GST?

Taking action on every IMS record is not mandatory; inaction results in deemed acceptance. If you change an action after the 14th, recompute GSTR-2B before filing GSTR-3B.

What is the 3-way invoice matching process in GST?

3-way matching compares three documents: the supplier invoice, the purchase order, and the Goods Receipt Note (GRN). All three must align on price, quantity, and delivery before the invoice is approved for payment and ITC is claimed.

What is 4-way invoice matching in GST?

4-way matching adds a quality inspection or acceptance report as a fourth verification layer. Used mainly in manufacturing and procurement-heavy industries to confirm goods meet specifications before approving payment and claiming ITC.

What happens if invoice matching fails under GST?

The invoice will not appear in GSTR-2B, blocking ITC for that period. The buyer must coordinate with the supplier to correct and re-upload it before the deadline under Section 16(4) of the CGST Act: 30 November following the end of the relevant financial year.

What fields are matched during GST invoice reconciliation?

Six fields are verified during reconciliation:

- GSTIN of the supplier

- GSTIN of the recipient

- Invoice or debit note number and date

- Taxable value

- Tax amount

A discrepancy in any one of these prevents ITC from flowing through for that invoice.