To address this, GSTN introduced the Invoice Management System (IMS) on 1st October 2024. It gives recipient taxpayers a structured, portal-based mechanism to review supplier invoices before those invoices affect their ITC claims.

This guide covers everything you need to know: what IMS is, how it works step-by-step, what each action means, which documents are covered, and how to prepare your business for compliance. It's particularly relevant for MSME owners, finance teams, and CA firms managing multiple client GSTINs.

Key Takeaways

- IMS is a GST portal facility where recipient taxpayers Accept, Reject, or mark invoices as Pending before they flow into GSTR-2B

- Inaction = automatic acceptance — invoices with no action are deemed accepted at GSTR-2B generation on the 14th

- Accepted invoices flow into GSTR-2B and auto-populate Table 4 of GSTR-3B for ITC claims

- IMS launched in October 2024 and is currently optional, but mandatory adoption is expected

- Review the IMS dashboard before the 14th each month to prevent unwanted GSTR-2B recomputation

What Is the Invoice Management System (IMS) Under GST?

IMS is a digital facility on the GSTN portal where registered recipient taxpayers can review B2B invoices, credit notes, debit notes, and amendments uploaded by their suppliers. For each record, the recipient can take one of three structured actions — Accept, Reject, or Pending — before it flows into their ITC claim.

The Problem IMS Was Built to Solve

Before IMS, buyers reconciled purchase registers manually against GSTR-2A or GSTR-2B. There was no formal mechanism on the portal to flag discrepancies to suppliers or dispute incorrect invoices systematically. The result: wrongful ITC claims, compliance notices, and disputes that could take months to resolve.

CBIC Circular No. 193/05/2023-GST documents how ITC tolerance rules tightened significantly — from 20% in October 2019 down to 0% from January 2022, when ITC became restricted strictly to invoices furnished by suppliers and communicated through GSTR-2B. IMS gives recipients a formal, portal-level mechanism to act on that verification rather than absorb whatever suppliers report.

Key Facts About IMS

| Detail | Information |

|---|---|

| Launch date | 1st October 2024 (available to taxpayers from 14th October 2024) |

| First IMS-based GSTR-2B | Generated 14th November 2024 (for October 2024 period) |

| Current status | Optional facility |

| Who can use it | All registered taxpayers, including QRMP filers |

| Legal basis | Section 38, CGST Act (amended via Finance Act 2025) |

IMS vs. E-Invoicing: Not the Same Thing

These two are frequently confused. E-invoicing is a supplier-side validation process — the supplier's system registers invoices with the IRP and gets an IRN. IMS is a recipient-side action layer — the buyer reviews what the supplier has reported and decides what flows into their ITC. Both are part of GST's digitisation push, but they operate at different points in the supply chain.

The Deemed Acceptance Rule

If a recipient takes no action on an invoice before GSTR-2B is generated, the system automatically treats it as accepted. Businesses that skip the IMS dashboard can unknowingly absorb incorrect or duplicate invoices directly into their ITC — with no easy way to reverse the impact after the return is filed.

How Does IMS Work? The Step-by-Step IMS Cycle

Step 1: Supplier Uploads Invoices

Suppliers file B2B invoices, debit notes, credit notes, and amendments through GSTR-1 (by the 11th), IFF, or GSTR-1A. Once submitted, these records automatically appear on the recipient's IMS dashboard under "Inward Supplies."

Step 2: Recipient Reviews the Dashboard

Access IMS via: GST Portal → Dashboard → Services → Returns → Invoice Management System

The dashboard classifies all inward records by document type and shows action status for each: No Action, Accepted, Rejected, or Pending.

Step 3: Actions Before the 14th Matter Most

GSTR-2B is auto-generated on the 14th of every subsequent month based on the current state of IMS actions. Key rules to know:

- Actions taken or changed after the 14th but before filing GSTR-3B require a GSTR-2B recomputation before filing.

- GSTR-2B can be recomputed as many times as needed before filing.

Step 4: IMS Feeds GSTR-2B, Which Feeds GSTR-3B

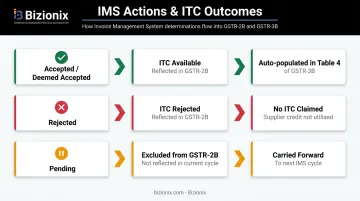

- Accepted / Deemed Accepted → flow into "ITC Available" section of GSTR-2B → auto-populate Table 4 of GSTR-3B

- Rejected → appear under "ITC Rejected" in GSTR-2B → contributes no ITC

- Pending → excluded from GSTR-2B for that month → carried forward to next IMS cycle

Once GSTR-3B is filed, accepted, deemed accepted, and rejected records are removed from IMS. Only pending records remain.

Step 5: Supplier Visibility and QRMP Rules

Suppliers can see the action status their buyer has taken on each invoice — accepted, rejected, or pending. That real-time visibility means both parties can identify and resolve mismatches directly on the portal, without waiting for month-end reconciliation calls.

For QRMP taxpayers, GSTR-2B is generated quarterly (GSTR-2BQ), not monthly. Months 1 and 2 of a quarter do not generate separate GSTR-2B statements; the combined GSTR-2BQ is generated on the 14th of the month following the quarter end.

The Three Actions in IMS: Accept, Reject, and Pending

Accept

Use this when the invoice matches your purchase records — correct GSTIN, amount, GST rate, and goods/services have been received.

- Accepted invoices are included in GSTR-2B and eligible for ITC in GSTR-3B

- If a wrong acceptance or rejection occurs before GSTR-3B is filed, it can be corrected — change the action and recompute GSTR-2B

Deemed acceptance reminder: Records with "No Action" are treated as accepted at GSTR-2B generation. Businesses not actively reviewing IMS will have invoices auto-absorbed into their ITC, including potentially incorrect ones.

Reject

Rejection is an active choice with specific downstream effects. Use it when an invoice is incorrect, duplicated, belongs to a different entity, or is unrelated to your business.

- Rejected invoices appear under "ITC Rejected" in GSTR-2B

- No ITC flows from rejected invoices

When a recipient rejects a supplier's credit note and files GSTR-3B, the system adds the corresponding GST liability back to the supplier's GSTR-3B in a subsequent period. Both parties should align before rejecting credit notes to avoid unexpected GST liability on the supplier's end.

Pending

Use this when:

- Goods or services have been invoiced but not yet received

- A discrepancy needs supplier clarification

- Supporting documentation is still under verification

Pending invoices are excluded from GSTR-2B and carried forward. Two limits apply:

1. Section 16(4) deadline: ITC must be claimed before the 30th of November following the end of the financial year to which the invoice pertains, or before filing the relevant annual return — whichever is earlier. Leaving invoices pending indefinitely risks permanent ITC lapse.

2. One-tax-period restriction (from October 2025): Certain specified records — including credit notes, upward amendments of credit notes, and downward amendments of invoices where the original was already accepted and GSTR-3B filed — can only remain pending for one tax period. After that window, if no action is taken, the system deems them accepted.

Which Documents Are (and Aren't) Covered Under IMS?

Documents That Appear in IMS (Require Action)

- B2B invoices

- Debit notes

- Credit notes

- Amendments to any of the above

These are reported by suppliers through GSTR-1, IFF, or GSTR-1A.

Documents That Flow Directly to GSTR-2B (No IMS Action Required)

- GSTR-5 records (Non-Resident Taxable Person returns)

- GSTR-6 records (Input Service Distributor invoices)

- Reverse Charge Mechanism (RCM) records

- Documents ineligible due to POS rules or Section 16(4) — these go directly to "ITC Not Available" in GSTR-2B

October 2025 Update: Bill of Entry Added to IMS

From the October 2025 tax period, GSTN introduced a dedicated "Import of Goods" section in IMS for Bill of Entry (BoE) records. Key rules for BoE handling:

- Recipients can Accept or mark records as Pending

- The Reject action is not available for BoE records

- No-action BoE records are deemed accepted at GSTR-2B generation, consistent with other IMS records

Knowing which documents require active review in IMS versus which auto-flow into GSTR-2B is essential. Treating all records the same — in either direction — creates compliance blind spots.

Key Benefits of IMS for Indian Businesses and MSMEs

ITC Accuracy and Mismatch Prevention

IMS ensures only verified invoices contribute to ITC claims. PIB reported that CBIC detected ₹36,374 crore worth of fake ITC across 9,190 cases in FY 2023-24. IMS gives legitimate businesses a tool to demonstrate they reviewed and approved each credit before claiming it — a meaningful protection during scrutiny or audits.

Audit Trail and Compliance Records

Every action in IMS is time-stamped. Auditors reviewing GST compliance can check accepted, rejected, and pending status per invoice without cross-referencing multiple files. Year-end reviews and notice responses become significantly more straightforward.

Working Capital Protection for MSMEs

Blocked or incorrectly claimed ITC directly affects cash flow — especially for MSMEs where receivables and tax credits are closely tied to operational liquidity. IMS gives finance teams a structured window to validate credits before they impact GST liability in GSTR-3B, avoiding unexpected tax outflows from ITC reversals.

Key advantages for MSME finance teams include:

- Early mismatch detection before credits are reflected in GSTR-3B

- Reduced reversal risk by confirming supplier filings before claiming ITC

- Cleaner audit records with a time-stamped accept/reject log per invoice

For MSMEs managing high invoice volumes, ERP platforms like Bizionix — built with integrated GST accounting and e-invoicing modules — keep purchase records aligned with GST return data, reducing the manual workload of IMS reconciliation.

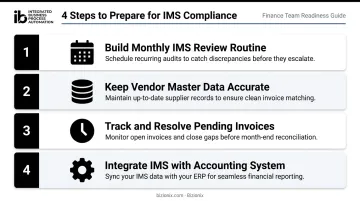

How to Prepare Your Business for IMS Compliance

1. Build a monthly IMS review routine

Schedule a dashboard review before the 14th each month. Actions taken before GSTR-2B generation avoid the mandatory recomputation step. After the 14th, you can still act — but you must recompute GSTR-2B before filing GSTR-3B.

2. Keep vendor master data accurate

Supplier GSTINs, trade names, and invoice details must match internal purchase records. Discrepancies at the data level make IMS reconciliation harder and increase rejections or disputes. A centralised vendor master — maintained within your accounting or ERP system — reduces this friction significantly.

3. Don't ignore pending invoices

Pending is not a long-term holding status. Track which invoices are pending, why, and when the Section 16(4) deadline falls. Build a review cycle that forces resolution within the financial year.

4. Integrate IMS actions with your accounting system

For businesses managing large invoice volumes, manual review of each IMS record is not realistic. A GST-compliant ERP like Bizionix — which supports GSTR-1 auto-population, GST return filing, and integrated purchase management — helps finance teams correlate IMS dashboard data with internal records systematically.

Bizionix also supports multi-GSTIN management from a single login. This is particularly useful for CA firms handling multiple client GSTINs who need to track IMS actions across different entities without toggling between separate systems.

Frequently Asked Questions

What is the Invoice Management System in GST?

IMS is a facility on the GST portal that allows registered recipient taxpayers to Accept, Reject, or keep Pending the invoices uploaded by their suppliers through GSTR-1, IFF, or GSTR-1A. It controls which invoices flow into GSTR-2B and ultimately which ITC is available in GSTR-3B.

Is the Invoice Management System needed for GST?

IMS is currently optional but strongly advisable. It gives taxpayers direct control over ITC accuracy and reduces mismatch risk. Finance Act 2025 amendments to Section 38 indicate mandatory implementation is coming, so businesses should begin adopting it now to avoid compliance gaps later.

When did IMS start in GST?

IMS was introduced by GSTN effective 1st October 2024 and became available to taxpayers on 14th October 2024. The first IMS-based GSTR-2B (for the October 2024 return period) was generated on 14th November 2024. It is available to all registered taxpayers, including QRMP filers.

What happens if no action is taken on an invoice in IMS?

If a recipient takes no action on an invoice, it is automatically treated as "deemed accepted" at the time GSTR-2B is generated. The invoice flows into GSTR-2B's ITC Available section as though the recipient had explicitly accepted it.

Can QRMP taxpayers use IMS under GST?

Yes. IMS is available for QRMP taxpayers, but their GSTR-2B (GSTR-2BQ) is generated quarterly — on the 14th of the month following the quarter end. Months 1 and 2 within the quarter do not generate separate GSTR-2B statements.

What is the difference between IMS and GSTR-2B?

IMS is the action layer: where recipients review and respond to supplier invoices. GSTR-2B is the output: the auto-generated ITC statement populated based on those IMS actions. IMS feeds GSTR-2B; GSTR-2B feeds GSTR-3B.